How To Fill In A Lean Canvas

When it comes to creating a new business, one question looms larger than all others:

“Does this have potential?”

There’s plenty of time to sort out partnership agreements, map customer journeys and create sophisticated financial projections…once you’re confident that people actually want what you’re selling.

If there’s no customer, or customers don’t see your products and services as being particularly interesting, then you don’t have a business idea on your hands.

Having said that, “Does this have potential?” requires a few pieces of information.

We need to think about our customer, what they’re looking for, what we offer them, how we serve them, how the numbers stack up, and why we think we can succeed where others have failed.

We need a way of capturing all of this on one piece of paper.

We need a Lean Canvas.

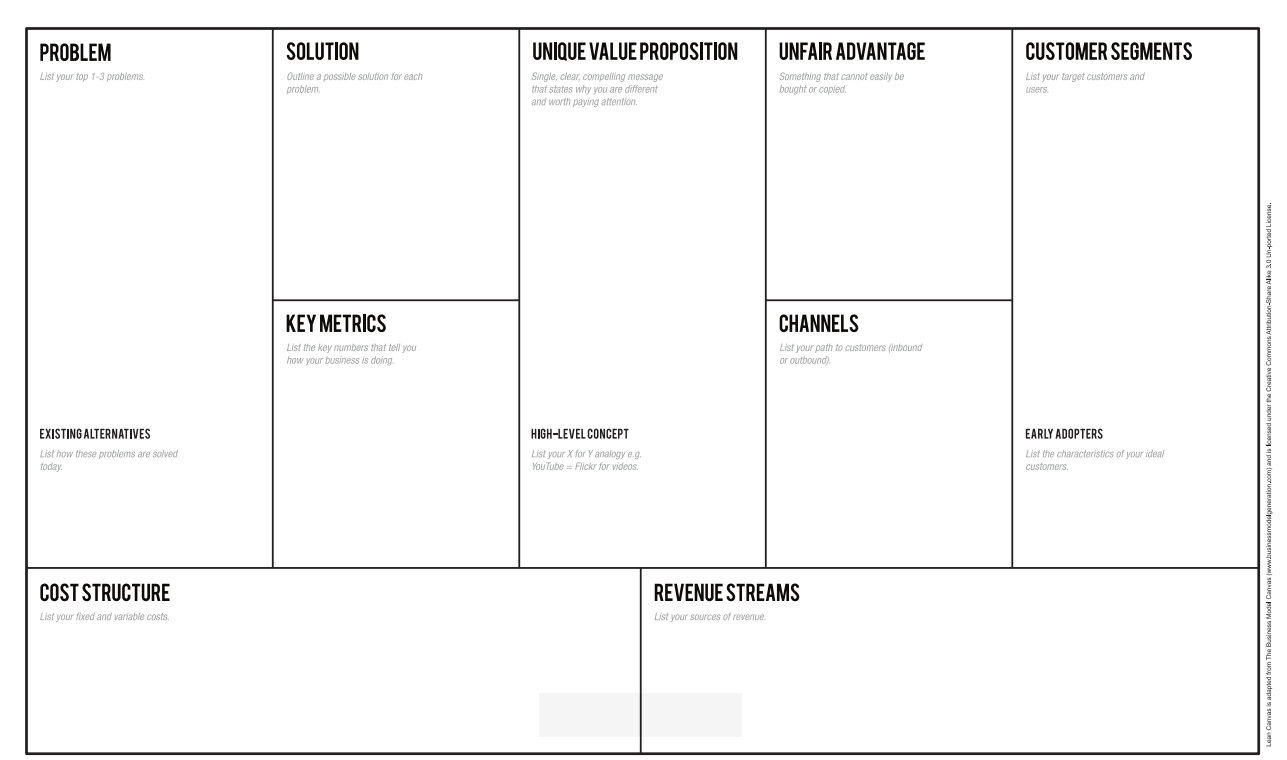

The Lean Canvas was adapted from The Business Model Canvas, swapping out some of the less urgent pieces like Key Activities and Customer Relationships, for more fundamental questions like Problem and Solution.

The two canvases can easily co-exist, since they do different things:

While a Business Model Canvas focuses on the Desirability, Feasibility and Viability, a Lean Canvas is primarily focused on Desirability and a bit of Viability.

This is particularly relevant for anyone who is still thinking about business ideas, rather than someone who works in a large company.

I encourage you to use both of them, but perhaps The Lean Canvas is a better starting point for new or evolving ideas.

The canvas is made up of nine boxes, each describing one aspect of your business idea.

You can download one here.

By seeing all these aspects on one page, we get a quick sense of the business and can start brainstorming ideas for tests or modifications.

I suppose you could fill the nine boxes in any order, but personally I’ve found this to be the easiest…

Customers and Problems

These two boxes are connected – we need to understand who our customers are and what is going on in their world.

The more specific we can be, the better.

Your business is not “for everyone”, it’s likely to have a few different types of customer, each with their own set of problems or ambitions.

We want to describe who each customer is, and what problems they feel like they have today.

When describing customers, we want to use a combination of demographics (age, geographic location, job description, income, etc) and psychographics (attitudes, worldviews, beliefs, identities, etc).

e.g. “We are selling to women between 40-65, who live within 10km of our shopfront and who see themselves as environmentally conscious.”

“We’re selling to people who love to cook at home and who care about food miles.”

“Our customers are school principals who are happy to trial an innovative program.”

We also want to describe the person who is making the purchase decision.

That means they either pay with their own money, or they are the ones overseeing a budget.

By contrast, the end user is the person who uses the product or service, but might not be the one who chose it.

For example, if you hire a new administrator who holds a vendetta against a certain airline, then suddenly that airline loses a lot of passengers in one hit.

That administrator is the real customer, and we need to understand how people like them choose what to buy.

Special attention goes to our Early Adopters – the group of people who will happily become the test audience for our new idea.

These people have a high tolerance for uncertainty, in exchange for being the first ones to try out your Unique Value Proposition.

These might be people you already know, people you can easily access, or customers who are particularly unhappy with the products available today.

It’s also worth mentioning – if you don’t think you know where the early adopters might be, then you should either do more research or pick a different customer segment.

Customers won’t appear in large numbers out of thin air.

When describing problems, we want to use the language of our customer – what do they see as being an issue or an incentive?

Sometimes these feel like negative states (our electricity bill is too high, washing the dishes takes too long), sometimes they feel like positive desires (I want to go on an adventure, I want a promotion at work).

This is really important – a startup can’t force customers to care about a problem, you have to tap into an existing interest.

Sure, a huge company can occasionally create a new problem (like how the makers of Listerine coined the term Halitosis for bad breath), but takes a lot of money and a lot of luck.

We want to sell something people want, and that means understanding what they want today and in the future.

Rob Fitzpatrick, author of The Mom Test, says it beautifully:

“It boils down to this:

You aren’t allowed to tell them what their problem is, and in return, they aren’t allowed to tell you what to build.

They own the problem, you own the solution.”

We can also use the Problems box to list the Existing Alternatives – the substitutes that our customers are using today.

These might be direct substitutes, like how Tesla is a substitute for Lexus, or an indirect substitute, like how a cinema is a substitute for live sport or live music.

Your customers are using some sort of alternative today, because if they’ve never tried to solve this problem, they’re either not your customer or this isn’t their problem.

e.g. If they haven’t tried to increase their physical activity before, they’re unlikely to care about your new fitness tracker.

Unique Value Proposition

It’s tempting to jump straight from problems to solutions, but this misses one of the most important ideas in all of business.

Customers don’t care about the technical details, they care about what’s in it for them.

A Value Proposition is the underlying reason someone buys something new or tries something different.

For example, one of the most compelling Value Propositions over the last century has been “your favourite music, wherever you are in the world”.

That applies to the gramophone, the cassette deck, the Walkman, the Discman, the first MP3 player, the iPod and Spotify.

Each of these used the best technology of the times to make this same offer, with a few nuances each time.

An early iPod owner might not have understood how MP3 compression worked, but they understood “1,000 songs in your pocket”.

A new business needs a Unique Value Proposition, one that helps it stand out from the crowd.

Think of it like this; why should someone take a risk and try something different?

What persuades them to overcome the switching costs?

What can’t they get from your competitors?

There needs to be a compelling offer, and one that makes customers happily hand over their money.

· Audible – great books you’ve been meaning to read, all while you drive/exercise/tidy up.

· Netflix – your favourite movies, on demand, with zero late fees.

· Illy pods– café-strength Italian coffee that fits in your Nespresso machine.

· YMCA Gyms – a gym you’ll actually use, since it’s on your way home.

· Casamigos – try George Clooney’s tequila.

· Nintendo Switch – portable, joyful entertainment for 1-4 players.

If customers don’t care about these Value Propositions, all the innovation in the world won’t help your company.

If George Clooney gets caught up in a Kevin Spacey style scandal, that tequila will lose its popularity.

Netflix no longer sends DVDs in the mail, but the Value Proposition is still essentially the same.

If I move across town, it doesn’t matter what my current gym installs, I’ll be cancelling my membership.

Solutions

Now we get to design products and services that deliver our Unique Value Proposition.

These are sets of features that customers pay for, in order to solve their existing problems.

Going back to our earlier music example, in 1980 the best solution was an eight-track cassette, and in 2003 it was a 4GB hard drive, now it’s a streaming service, and in the future it could be an implant.

We can brainstorm and test several different solutions for the same Value Proposition.

For example, let’s say customers are students who feel lost when it comes to choosing a career:

· You could start a podcast that interviews successful people with unusual backgrounds.

· You could start a career counselling service with physical branches.

· You could create a Tinder style app that lets you swipe on different jobs that match your skills and preferences.

· You could write a series of books about career pathways in different industries.

The key here is to try and generate lots of ideas, and check them with real customers.

It’s also worth thinking about which types of solution are easy to monetize, since that early income is going to fuel your startup’s development.

Channels

Your soon-to-be-loyal customers don’t yet know that you exist.

That means you’re going to have to do something to get in front of them.

You can run Instagram ads, or a pop-up in a busy area, or go door-knocking in your neighbourhood, or create sponsored content on a popular platform.

Once they know about your brand, your products and your Value Proposition, you can then choose a method of delivering your solution to them.

These might be different channels, e.g. advertising through Google, then sending parcels in the post.

For example, toothbrush company quip advertised heavily through podcasts, then deliver new brush heads to customers every few months.

Fresh Prince of Baklava attract new customers via Instagram, then hand deliver treats to your door.

Amazon lets you choose ebooks through their online store, then download them straight to your device.

Remember, you don’t need to invent a new channel, you want to pick the existing channels that best match your customer and Unique Value Proposition.

Revenue Streams

The difference between a business and a hobby is revenue.

If your users aren’t paying for your services, they’re either your fans or your product, but they’re not really customers.

Money needs to change hands; it proves that they genuinely value the problem you’re solving, and cash is vital for growing your startup.

Some new entrepreneurs get weird about asking for payment, but there’s no choice – we need to generate revenue.

That said, you have lots of choices and can get a bit creative.

Revenue streams include:

· Selling a product (Fitbit activity trackers)

· Selling a service (Amazon Web Hosting)

· Selling access to a shared resource (Netflix content library)

· Selling membership to a club (F45 gyms)

· Selling advertisements to your audience (Instagram)

· Licensing your intellectual property (Marvel and their characters)

· Agent or Broker fees (Airbnb fees)

There aren’t “Good” or “Bad” revenue streams, it all comes down to the context of your industry and audience.

Subscriptions might be a good idea.

Microtransactions might be a good idea.

Free trials might be a good idea.

Giving the core product away for free might be a good idea.

Franchising might be a good idea.

Partnerships might be a good idea.

Bundles might be a good idea.

Try all your options as thought experiments, then as real world experiments, and see what you like.

Cost Structure

All of these promises around Value Propositions and Solutions come at a price, as do your Channels.

We want to understand where our money will get spent when serving a customer, to ensure that we’re consistently making a surplus.

We don’t need detailed financial models, we just need to identify where and when our money gets spent.

What will be the main expenses for your business?

Cost of goods?

Research and innovation?

Staff salaries?

Licensing fees?

App development?

Rent?

Running your sales channels?

For example, an online-only business will have very different costs to a vegan café.

A pharmaceutical company will have much higher upfront costs than a drop shipping business.

You want to use this box to get a sense of when you will break even – at 10 customers, 1,000 customers or 1,000,000 customers?

Key Metrics

A big question for all of the other boxes on the canvas is “How will we know this is working?”.

How will you measure your customer base and their behaviour?

How will you measure the effectiveness of your solution?

How will you measure your financial performance?

How will you measure your social impact?

How will you measure your traction?

Some companies will focus on Daily active users, other focus on retention rates, or maybe the percentage of customers who appear satisfied.

You might measure how many customers refer a friend, or how much money each customer spends in the first month.

The trick is to measure the numbers that matter, not the “Vanity Metrics” that look great but don’t mean very much.

For example, measuring user behaviour, success rates and revenue are more important than clicks, views, shares and awards, even though the latter feel pretty nice.

If you get lots of signups but then lose those customers straight away, this is a huge warning sign that something isn’t working and requires your urgent attention.

A suggestion from the great book The Four Disciplines Of Execution:

You want a leading metric and a lagging metric.

Leading metrics measure your activity before results are visible, whereas lagging metrics capture the gradual changes that take time to appear.

Individually they paint a very biased picture, but together they bring clarity.

Unfair Advantage

Generally speaking, you’ve picked a concept that either nobody has thought of, or they deemed impossible, or they tried but couldn’t quite make it work.

That shouldn’t put you off, but it should make you ask: What are we going to do differently?

It could be something like:

· Better timing

· Better technology

· A world class founding team

· Access to a large pool of resources

· Access to a large pool of customers

· Access to a large pool of intelligence/data

· Great branding

· Top notch salespeople

· Unique partnerships

· Favourable policies in your country

Think of how Tesla managed to succeed where other electric cars failed.

How Nespresso became so much more popular than their earlier Dolce Gusto.

Why the iPod beat the Zune so convincingly.

What gives Richard Branson an edge in any new market Virgin enters.

Why Zoom was able to overtake Skype’s 17 year head start.

You don’t need the backing of a billion dollar company, but you want to think about why you would be able to succeed where your competitors haven’t (or won’t in the future).

So now we have the nine boxes filled in.

How do we go from “Yeah… it’s a canvas” to “Hey this might be a great business”?

Connecting The Boxes

We want our canvas to tell a compelling story, and that means the pieces need to fit together.

Specifically, the customers we describe on the right need to match the problems on the left.

They need to care about the Unique Value Propositions in the middle.

The solutions we’ve designed need to be able to make those Value Propositions a reality.

The channels need to lead us to a substantial pool of customers.

Customers must be willing and able to pay for these Value Propositions, through the Revenue Streams outlined at the bottom.

These revenues need to outpace our Costs, or else we’ll never break even.

The Key Metrics need to describe our customer’s enthusiasm, both through their spending and whether or not they get the Value Proposition they’re looking for.

Our Unfair Advantage has to be real, and relate to at least one other part of the canvas.

Validation Through Experiments

These boxes are full of guesses, at least for now.

We want to replace those guesses with evidence, and that come from validating each point with an experiment.

For example, we can use pre-orders to validate that our customers are real and that our prices are acceptable.

We can create a prototype to see if our solutions can genuinely deliver our Unique Value Proposition, and to see if our Cost Structure is realistic.

We can conduct customer interviews to see if people genuinely care enough about these problems to pay for a solution.

We can trial a series of solutions, to see if our Unfair Advantage is real, or if there are multiple ways of serving our customers.

Remember, a failed experiment is a success – it saves an incredible amount of time, money and energy, and gives you insights that will lead you towards a model that genuinely works.

Keep Iterating

As good as this canvas might look, we don’t want to fall in love with our first idea.

Good ideas survive competition, and by creating and testing lots of ideas, the great ones rise to the top.

This doesn’t have to be hard work – you can start by changing one or two elements of the first Lean Canvas.

For example:

· Keep the customer the same, but focus on a different problem

· Keep the problem the same, but focus on a different customer base

· Keep the same Unique Value Proposition, but focus on a different solution

· Keep the same Unique Value Proposition, but focus on different revenue streams

· Use totally different Channels, like doing everything online or everything in person

· Focus on a different part of the Value Chain

· Use a combination of existing solutions to solve a customer’s problem

What usually happens is that you discover that most alternative models don’t work…but two or three might.

This means you go into your next round of validation and prototyping with three good ideas, taking the emotional attachment away from that first idea and making you a better judge of their potential.

Talk To Your Trusted Advisors

This next step is super important: you want to bounce your ideas off the right people in the right way.

It’s so easy for this to go wrong, either by talking to negative/discouraging people, or wildly optimistic people.

Both of them are unhelpful.

What you want is a sounding board who will ask good questions and offer interesting ideas.

These are people who use Can-If suggestions to problems, who encourage you to keep going, and who can introduce you to other knowledgeable people.

You don’t need to create Non-Disclosure Agreements, you don’t need Devil’s Advocates, you don’t need to raise money.

Instead you want a balance of enthusiasm and realism, pushing you to keep going.

More Great Tools

Now that you’ve got a decent Lean Canvas (especially once you’ve made a few), here are the next great tools to help clarify and strengthen your business:

Customer Journey Maps – these help you design seamless experiences, win over new fans and re-engage your old customers.

Value Proposition Canvases – go in-depth into customers jobs, pains and gains.

Test Cards – design objective experiments that confirm or disprove your assumptions.

Can If Maps – creative ways to make tricky ideas possible.