Business Model Expiration Dates

“There’s a startup somewhere making bullets with your company’s name on them”

Australia’s headlines have been dominated by the news that carmaker Holden will be withdrawn from the market, after 164 years.

Plenty of businesses are entering administration these days, but the Holden one has caught people off guard – including the Prime Minister.

Holden is owned by General Motors, and was one of the most popular car brands over the 20th century; I’ve met people with Holden tattoos.

Without wanting to dance on their grave, their departure is also completely understandable – I don’t know anyone who has bought a Holden in the past seven years, and they stopped manufacturing cars here in 2016.

Still, an iconic brand leaving the country is a great reminder of this innovation principle: every business model has an expiration date.

Longevity does not guarantee permanence – although it can certainly give you a fighting chance.

Every business has to delight it’s customer (even if they don’t delight their end users), or else it won’t be long before customers look elsewhere.

From a cashflow perspective, every business needs to be constantly delighting customers – either by finding a new audience each year or by servicing an existing customer base.

In other words, you should be able to answer the question “Who have we delighted lately?”.

Delight usually comes from some form of competitive advantage; something that the market can’t get from your competitors.

It might be that you’re cheaper than others.

It might be that you’re better than others.

It might be that you’re more convenient than others.

Every business should be able to articulate why their customers pick them over their rivals, even if the reason isn’t noble or flattering.

Over time these competitive advantages are liable to change – it could be because customers change, or technology changes, or because a new entrant comes in with an even more impressive offer.

It’s possible to change your competitive advantage over time, but it takes a great deal of insight, preparation, luck and effort.

Holden themselves are a great example of this, in 1856 they were in the carriage business, not motor vehicles.

Their carriage-making credentials and insights helped them create cars that were both high quality, stylishly designed and well-priced, making them a nation’s favourite.

That said, their credentials and insights from the 1950’s did not translate into the 2020 market, where they are competing with the efficiency of Korea and brands like Tesla.

I can’t imagine anyone got a Holden tattoo recently.

General Motors probably made the right call, as devastating as it was to their employees.

Australia is not a market where they can win, so maybe doubling down in their larger markets is for the best.

On the other hand, for the rest of us without huge multinational businesses, here are some practical steps you can take to re-design your business model:

Rethink your Customer Segments and Value Propositions – The Offer

People are right to take the best offer available, they’re not being disloyal, they’re being sensible.

What constitutes “the best offer” will continue to change over time – what your parents looked for in a car will be different to what you look for, which will be completely different to what your kids look for (the entire concept of car ownership may well be obsolete by then).

The customer of 2015 had a different set of Jobs To Be Done, a different level of sophistication (for better or worse), a different set of expectations and a different budget.

This is one reason why I recommend that you don’t outsource your customer testing – you need a good look at today’s customer if you’re going to speculate about your future raving fans.

It’s also worth tracking the offers made by your direct competitors and indirect competitors – who are they targeting, what language are they using, what are they highlighting in their offers?

Finally, try mentally starting from scratch – if you didn’t have this business today, who would you want to serve and what offer would you pitch to them?

Rethink your Customers Relationships and Channels – The Shopfront

Sometimes the offer might not change, but the shopfront could look completely different.

A very recent example is the rise of the neobank, a term I heard for the first time last month, describing a new set of digital banks like Xinja and 86400.

Having searched their names on Google, I have since been constantly retargeted through social media advertising, to take up a loan or savings account without ever needing to talk to a real person or step into a branch.

The fundamentals of banking are the same, the offer is generally the same (better interest, lower fees, convenient), but the shopfront is now entirely based on my phone.

Amazon is a great example, moving book sales online and then back to physical retail stores (but only in some markets).

A book is a book, but Amazon have made it available on their own platforms like Kindle and Audible, attracting a different crowd to those who were happy with brick and mortar bookstores.

The same principles are behind the field of telemedicine – assistance without the need for long distance travel.

This has huge potential for fields like psychology (where people can access support while in a bad state) or diagnostics (where patients can access top specialists who may be on the other side of the world).

Rethink your Resources, Activities and Partners – The Engine

Some offers remain pretty much the same for decades, but the way the company runs may change completely.

The fundamentals of insurance are the same today as they were hundreds of years ago, but now insurers advertise their secret weapon; the absence of staff.

That’s right, not having a team behind the scenes is pitched as a strength, and is helping them offer better prices.

Journalism is another industry going through this shift, no longer dependent on the same workforce that they used throughout the 20th century.

News is delivered digitally, with teams focused on clicks, impressions, alerts and eyeballs rather than printing and distribution.

Collaboration is changing industries like fashion, whereby retailers can form rapid partnerships with other brands to create something new and exclusive.

These team-ups keep both parties relevant, without needing to enter a new industry.

Another great example of this is the changing workforce – automation is changing the roles we need to fill, and remote work arrangements allows us to hire from previously inaccessible talent pools.

Rethink your Cost Structures and Revenue Streams – The Margins

Cashflow is a huge headache for many businesses, so there’s a growing interest in business models that allow a company to earn before they spend.

A great example of this is crowdfunding or pre-sales, where a company can test a new product/service with the market without needing to invest huge sums in factories and research.

The marketing acts as the research, so the business only has to build the offers that entice customers into opening their wallets.

Another example is the move towards outsourcing, whereby a company can buy finished products from a specialist, removing the need for expensive R&D.

e.g. you can start your own supplement or cosmetics company by hiring someone to “white label” the goods which you then brand as your own.

The price per unit might be cheaper if you made them all yourself, but that would require a huge outlay of cash, and you’re not necessarily an expert manufacturer so there’s more risk.

Customers continue to change how they like to pay for products and services; music and television shows are now mostly via subscription, whereas news is expected to be free but with targeted advertising.

Price sensitivity is also changing - $2,000 is no longer considered an unrealistic price for a phone, while 60GB of mobile data is expected to cost less than $60 per month.

Ubers are cheaper than taxis, yet Uber Eats is more expensive than in-person dining.

The margins of the ‘90s are likely to be different to the margins of the 2030s; you’re welcome to find that out the easy way or the hard way.

They say it’s better to worry a little today instead of worrying a lot in the future.

Perhaps it feels paranoid now, but a little fear could save your business from becoming obsolete.

Here are three healthy fears that should prompt your new ideas:

A healthy fear of big businesses

Could a large company decide to spend the money tomorrow and re-create your entire business in one go?

Are the components readily available for someone with money?

This is the “moats” question that investor Warren Buffett looks at when analysing a business – what makes it hard for someone else to replicate their success?

The idea here is to dig a moat around your company, making it hard for others to capture.

Examples of moats are your reputation, your staff, your equipment, access to scarce resources, partnerships with other suppliers, or an extensive network of customers.

A moat is what leads to a larger company trying to acquire you (at a lucrative price), rather than trying to run you out of business.

A healthy fear of startups

One of my favourite questions to ask larger institutions is “what would a startup do to solve this problem?”.

It turns out that startups are scary for institutions because they’re not stuck with all of the systems, processes and overheads that usually slow down the pace of change.

A startup can trial, promote, sell and pivot an idea in a number of weeks, while the bigger company would barely have finished their feasibility study.

These startups are often able to offer the latest technology, lower prices, personalised services, cheekier brand messaging and come across as a breath of fresh air.

Larger organisations often have cultures that discourage risk-taking, wanting to see concrete evidence of an idea’s merit before committing any time and money to it.

That often pushes out the creative and motivated people to start their own rival ventures, where they can run experiments without waiting months for “permission”.

A healthy fear of inner turmoil

One of the most common causes of dysfunction is inner turmoil amongst a team.

You can beat your competitors in the market, but if your culture is toxic then it will soon affect your systems, your decision making and eventually your services.

This pushes out great people, discourages collaborative partnerships, and makes top talent look elsewhere.

A lack of trust means that product managers fight instead of constructively supporting each other, so more time gets spent on politics than on innovation.

This can be invisible to the outside world for a while, but it silently hollows out once-great companies from within, making them incredibly vulnerable to small changes in the future.

If you want to avoid your business model’s expiration date from being an issue, then you’re going to need to be proactive.

Proactive innovation takes humility and curiosity – and a genuine love for what you do.

It means taking the time to think about how you might create something 10x better than what you make today, without becoming defensive and shutting down the thoughts out of discomfort.

It means removing today’s constraints from tomorrow’s possibilities.

For example, the NBA originally didn’t have a rule against goaltending (blocking the ball from going in the basket) because they thought it was impossible to do (who could get up that high?).

Their assumptions were wrong – a 7 foot 5 player could easily jam up the ring and allow zero points to the opposition, but back then a 7 foot 5 person was a ridiculous concept.

We can’t assume that today’s constraints will be in place in 20-30 years’ time, but should instead focus on what’s unlikely to change.

Bill Bernbach called these “simple, timeless human truths”, and considered them the template for good advertising.

e.g. what are your grandchildren likely to prioritise when they start shopping for themselves?

The products and services will be different, but the Value Propositions are likely to be the same as before.

Another way of thinking is to imagine that you were your own competitor.

How might you create a better offer?

How might you create a better shopfront?

How might you create a better engine?

How might you create better margins?

These questions work because they harness your creativity towards new ideas, rather than towards finding reasons to avoid change and risk.

The thought of an expiring business model can make people feel uneasy or excited, and both feelings are best channelled into good creative tools.

For thinking about customers and offers, I highly recommend the Value Proposition Canvas.

For thinking about business models, I highly recommend the Business Model Canvas.

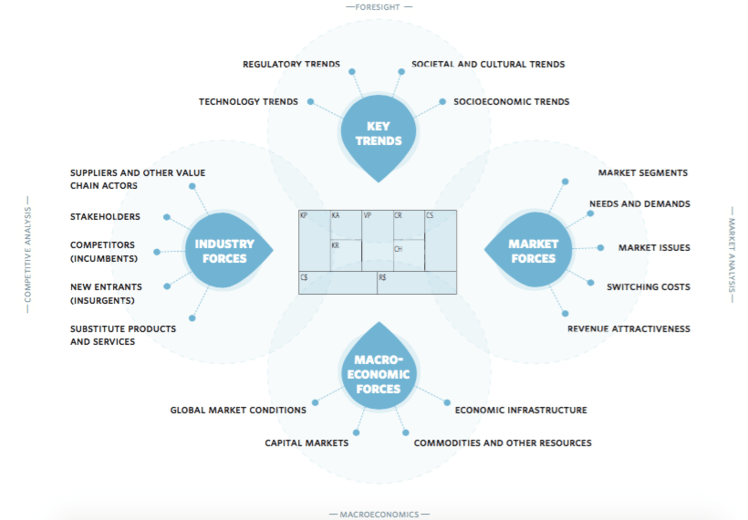

For thinking about your industry, I highly recommend the Business Model Environment.

For testing new ideas, I highly recommend the Strategyzer Test Card.

For overcoming your natural pessimism, I highly recommend the Can If Map.